The Ultimate Guide To Hsmb Advisory Llc

Table of ContentsHsmb Advisory Llc Things To Know Before You Get ThisThe Of Hsmb Advisory LlcThe Facts About Hsmb Advisory Llc RevealedNot known Facts About Hsmb Advisory LlcHsmb Advisory Llc Fundamentals ExplainedIndicators on Hsmb Advisory Llc You Should KnowSome Of Hsmb Advisory Llc

In either case you should get a certification of insurance coverage defining the provisions of the group policy and any type of insurance fee. Generally the maximum quantity of coverage is $220,000 for a mortgage and $55,000 for all other debts - https://www.bitchute.com/channel/qoDZnaBaBWar/. Credit scores life insurance coverage need not be purchased from the company providing the funding

Facts About Hsmb Advisory Llc Uncovered

However, home collections are not made and costs are mailed by you to the agent or to the firm. There are specific factors that have a tendency to increase the expenses of debit insurance greater than normal life insurance policy strategies: Certain expenditures coincide no issue what the size of the plan, so that smaller policies issued as debit insurance policy will have greater costs per $1,000 of insurance than larger dimension regular insurance plan.

Because very early gaps are expensive to a business, the prices must be passed on to all debit insurance holders. Since debit insurance coverage is created to consist of home collections, higher compensations and charges are paid on debit insurance policy than on regular insurance. In most cases these greater expenses are passed on to the insurance policy holder.

Hsmb Advisory Llc for Beginners

Where a firm has various costs for debit and normal insurance coverage it might be possible for you to purchase a bigger quantity of routine insurance coverage than debit at no extra cost. If you are thinking of debit insurance policy, you need to definitely examine regular life insurance policy as a cost-saving option.

What Does Hsmb Advisory Llc Mean?

Joint Life and Survivor Insurance coverage supplies protection for two or even more persons with the survivor benefit payable at the fatality of the last of the insureds. Premiums are dramatically reduced under joint life and survivor insurance coverage than for policies that guarantee only one individual, given that the likelihood of having to pay a fatality claim is reduced.

Premiums are considerably higher than for policies that guarantee one person, because the likelihood of needing to pay a death claim is greater. Endowment insurance supplies for the payment of the face amount to your recipient if death occurs within a details amount of time such as twenty years, or, if at the end of the specific duration you are still alive, for the payment of the face total up to you.

Juvenile insurance coverage provides a minimum of security and could provide protection, which might not be offered at a later day. Quantities offered under such protection are generally limited based upon the age of the kid. The existing limitations for minors under the age of 14 (https://papaly.com/categories/share?id=500bfb4b6d14494f860b638ecffc18c8).5 would be the higher of $50,000 or 50% of the amount of life insurance policy in force upon the life of the applicant

Getting The Hsmb Advisory Llc To Work

Juvenile insurance may be marketed with a payor advantage biker, which gives for forgoing future costs on the kid's policy in the event of the fatality of the individual that pays the premium. Elderly life insurance coverage, often described as rated survivor benefit strategies, offers eligible older applicants with minimal entire life protection without a medical checkup.

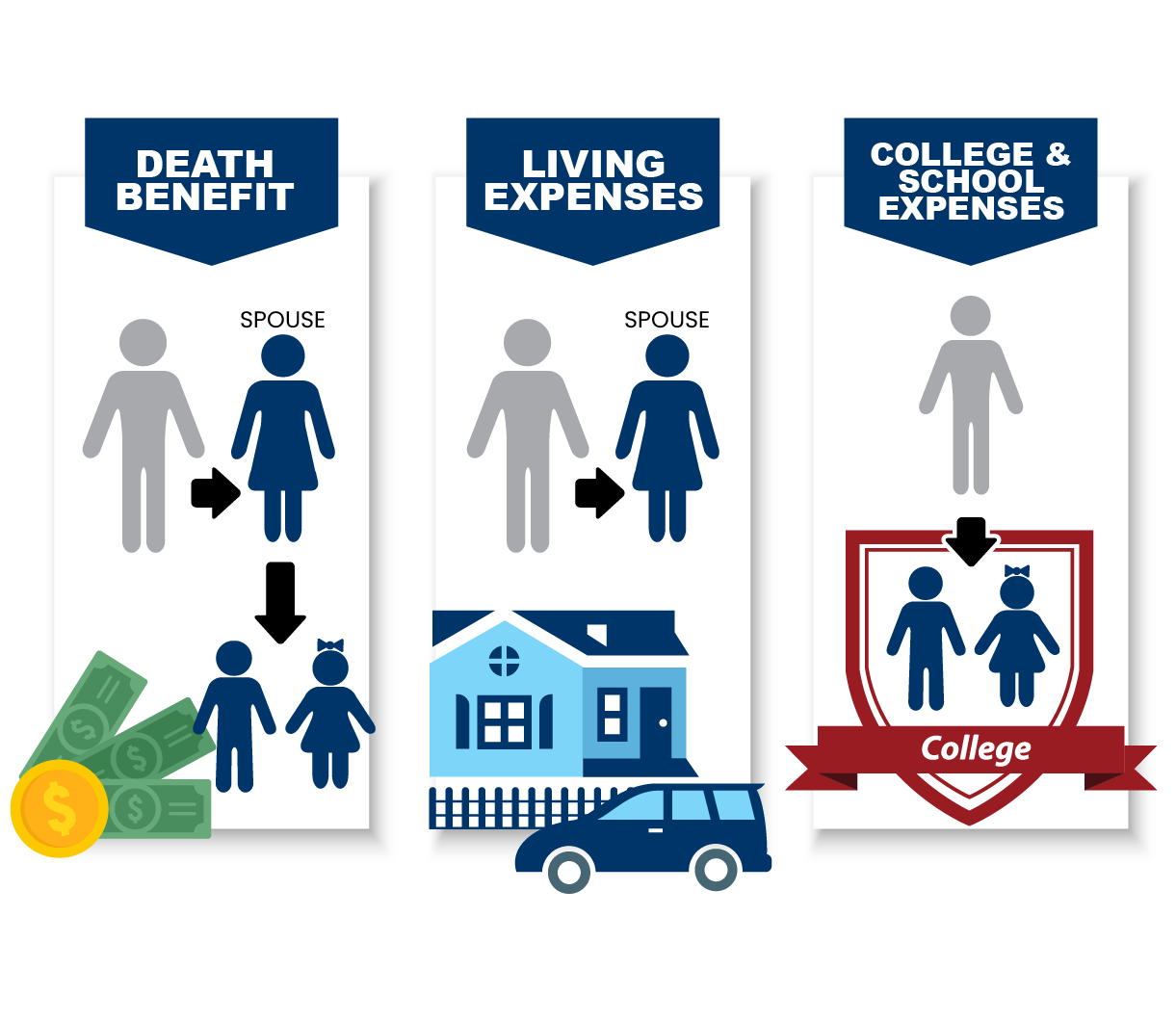

The purpose of life insurance is quite easy: in the occasion of your death, life insurance will certainly offer insurance coverage for your household and loved ones to guarantee their financial protection. Nevertheless, life insurance policy benefits differ by policy kind and each life insurance strategy offers its very own collection of advantages for the plan holder.

Flexible term lengths that can be tailored based both on your family's requirements and spending plan. The option of transforming to a Whole Life insurance policy policy. Lifestyle Insurance Policy offers protection that you can make use of throughout your lifetime. The benefits of High quality of Life Insurance policy include: Versatile and economical term prices Top quality of Life Insurance coverage are not only budget friendly since they cover several requirements, yet they can additionally be gotten used to accommodate certain events in your life and enable you to access see here now the money advantage of your plan.

Some Of Hsmb Advisory Llc

For more information, go here. Protection for medical costs and costs. Whole Life Insurance Policy has no insurance coverage expiry date it lasts your whole life. You simply acquire the policy coverage and maintain paying the same costs rate throughout your working and retirement years. The advantages of Whole Life Insurance consist of: Adjustable insurance coverage that can be altered as your demands alter.

To learn more, go here. There are additionally some unforeseen advantages of life insurance policy where your life insurance plan can cover scenarios and functions you could not have taken into consideration. Life Insurance St Petersburg, FL. Here are a few unexpected advantages of life insurance policy: If your companion is currently solely accountable for your children, your life insurance coverage policy can assist them spend for childcare or one more childcare service while they go back to function.

The objective of life insurance is pretty easy: in case of your death, life insurance policy will offer protection for your household and liked ones to ensure their financial safety and security. However, life insurance policy benefits vary by plan kind and each life insurance policy strategy supplies its very own set of benefits for the plan owner.

More About Hsmb Advisory Llc

Versatile term sizes that can be customized based both on your household's demands and budget plan. The choice of transforming to a Whole Life insurance policy policy. Lifestyle Insurance offers protection that you can make use of throughout your life time. The advantages of Quality of Life Insurance coverage include: Adaptable and economical term prices Lifestyle Insurance coverage are not just inexpensive considering that they cover multiple needs, however they can also be gotten used to accommodate certain occasions in your life and enable you to access the cash money benefit of your policy.

For more details, click here. Coverage for medical bills and expenses. Whole Life Insurance Policy has no protection expiry day it lasts your entire life. You just purchase the policy coverage and keep paying the same costs price throughout your working and retirement years. The benefits of Whole Life Insurance include: Flexible insurance coverage that can be transformed as your requirements alter.

For more details, go here. There are additionally some unforeseen benefits of life insurance where your life insurance policy policy can cover scenarios and objectives you may not have taken into consideration. Below are a few unanticipated benefits of life insurance: If your companion is now solely in charge of your kids, your life insurance policy plan could aid them pay for childcare or one more child care service while they go back to work.